Sometimes You Just Need to Jump

“You don’t have to be great to start, but you have to start to be great”, is one of my favorite quotes from Zig Ziglar. Whether we are discussing fitness goals, a career change or a financial plan, new habits are hard to start and even more difficult to maintain but most people never even venture close enough to life’s edge to jump. We make the excuse that “we’ll get around to it” or “start next week”. However, as Napoleon Hill reminds us, “Those who will not take a chance seldom have one thrust upon them.” Sometimes you just need to jump!

“Those who will not take a chance

seldom have one thrust upon them.”

For me, this post is my jump. I postponed this numerous times, busying myself with everything except writing, and each time strategizing how I will “really get after it” the following week. The thing is, we all struggle with a fear of the unknown. We might be incredibly bold or disciplined in one area but lack the confidence or experience in another, and we just need to start.

So perhaps as you read this, there is something you’ve been putting off or waiting for the right time to begin. Take this as a gentle nudge, sometimes you just need to jump! And as you launch, remember there will always be obstacles, but as John Maxwell puts it, “where there is hope in the future, there is power in the present!”

Make it a great week!

What is “Fee-Only” and Why Advisor Compensation Matters

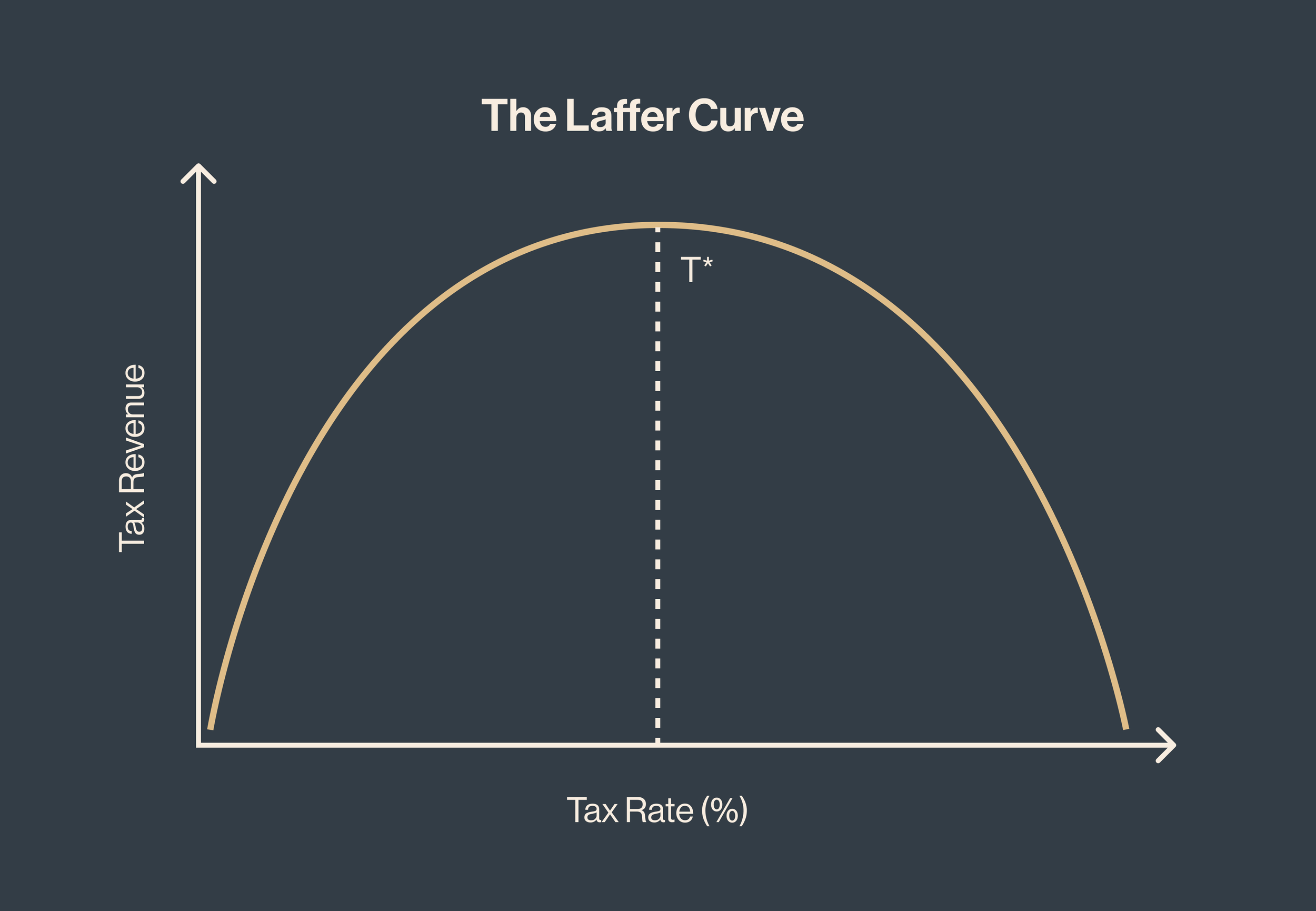

Incentives matter. Ask any economist, CPA, or Sales Executive and they will all share with you the power of incentives in motivating behavior. For example, the Laffer Curve was revolutionary in keenly depicting how increasing taxes beyond a certain threshold disincentivizes taxpayers to work, thus reducing total tax revenue:

Yet somehow, in the financial services industry, clients have been led to believe that incentives don’t matter, that you can trust an advisor to provide sound advice while they are financially incentivized to sell commission-based products and transfer assets to expense-laden proprietary mutual funds.

Undisclosed Incentives

You may ask, where is the client in all this and how are they truly being served? Isn’t there a conflict of interest that should be disclosed? Yes! But because of the length and complexity of these disclosures, the average investor simply signs the agreement, trusting the advisor to act in a manner inconsistent with their incentives. Some clients do understand the conflict of interest and proceed simply because they don’t know of another alternative for investment advice.

The Solution: Aligned Incentives

So, what’s the solution? Is there an alternative to working with an advisor you keep at arms-length, never sure if their products or services are in your best interest? There is a subset of advisors that provide fee-only, fiduciary advice and whose sole compensation comes from you, the client. No commissions, hidden fees, load funds, or kickbacks. Not only does this reduce conflict of interest, but it also aligns incentives.

This is why choosing a “fee-only” advisor is so important. While it may be uncomfortable to ask your advisor how they are compensated, it’s far more uncomfortable not knowing if you can trust their advice or discovering after 20 years that you’ve lost $75,000 in hidden fund fees. While managing finances can be challenging, managing who your financial advisor is should be simple. Advice should be straightforward and compensation transparent, free from hidden fees.

The following resources may be helpful if you’re looking for a “fee-only” advisor: